In our recent analysis on The Legal Marketplace in a Post-COVID World, we predicted a significant uptick in law firm merger activity once the immediate medical crisis was brought under control. For larger firms, this will be driven by a “significant new focus on talent, scale, depth and redundancy… particularly among firms focused on multinational/jurisdictional client bases.” For smaller firms, we are hearing increasing interest due to pressures such as significant concerns with talent/generational gaps in key practices or around key clients, the lack of future leaders, insufficient capitalization (for when the next major unexpected event hits), and general poaching pressures from larger, more profitable competitors.

We are already seeing this expected uptick in inquiries to our law firm merger practice (aka LawVision MergerCounsel) from law firm leaders who see opportunity on the horizon and we want to help manage the expectations of those who may be experiencing some combination of the factors listed above. To that end, we offer a data-focused primer based on our law firm merger practice. In this piece, we are not going to provide broad generalizations about how all law firm mergers work because, in our experiences across three decades, we have found that each proposed combination is a unique event that features some new twist or turn. Therefore, we are going to share some of the high-level details from our most recent 30 law firm merger engagements – projects that we have been involved with over the past 2 years – and summarize our experiences. Based on real examples, we hope to (re)set or manage your expectations if you are relying on a merger or acquisition to implement a strategy or solve a problem.

We are not going to use any law firm names, nor are we going to describe in detail any proposed law firm merger that involved a unique and identifiable trait, characteristic, or outcome. Confidentiality is vitally important in all aspects of merger counseling.

Before proceeding into our summary, it is important to understand the underlying data set. The 30 potential combinations we are reviewing are those potential transactions that were deemed worthy (by both parties) of the investment of time and money to seriously explore a formal combination. Based on our preliminary assessment work, each of these proposed transactions had a strategic foundation, support from both leadership teams, reasonably close economics, and was free of deal-killing conflicts before it reached this stage. From a pure numbers perspective, it is important to note that for every one of these truly viable potential mergers there are, by our rough estimates, 9 other concepts/discussions/ideas that go nowhere. In other words, to get into one substantive conversation, you may need up to 10 preliminary conversations. (We’ll talk about the 9 out of 10 that go nowhere in a future article.)

Now, let’s look at these 30 law firm merger projects as a group to see what happened.

To prepare this analysis, we summarized key data points that we track for each proposed combination that align with questions that we are routinely asked regarding our M&A practice. As such, the following observations summarize the results of the one-in-ten conversations that became a serious attempt to structure a merger or acquisition between two interested parties:

What was the goal/primary reason for trying to merge the two firms?

To calculate this, we used two data fields in our records – the primary goal and the secondary goal for the transaction. A primary goal was assigned two points and a secondary goal was assigned one to create a weighted scoring approach. For each category, we summed the points from both categories to produce our top three categories, in descending order:

-

- Implement a strategic objective (35 points)

- This is not “growth for growth sake”. This is usually to create longer-term breadth or depth where needed and not readily available within the current organizations or to extend geography in ways consistent with clear strategic goals.

- Prepare for generational shifts (24)

- This is where firm leadership looks five years into the future and sees developing talent gaps that, over time and due to retirements, will put key practices and/or client relationships at risk.

- Add needed depth to important practices (18)

- This is where firm leadership looks at the current situation and sees existing talent gaps and/or the immediate need for additional resources to meet existing demand.

- Implement a strategic objective (35 points)

Below these top three, there are several “one-off” categories that paled in scoring comparison to these top three.

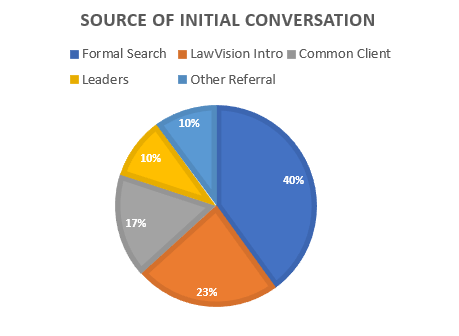

What was the source of the initial conversation?

- Formal targeted search by either party – 12 of the 30 firms

- This is where one or both parties were developing specific “target lists” of candidate firms that met their goals (above).

- LawVision was involved in developing seven of these target lists.

- LawVision introduction – 7

- Through our MergerCounsel service, we are regularly on the lookout for deals that may make sense for our clients who take a more opportunistic approach rather than conduct a formal search. From our regular MergerCounsel database reviews and brainstorming meetings we sometimes connect the dots between two firms that make great sense.

- If you wish to be in this general flow of confidential reviews and discussions at no charge (unless we bring you a concept that results in a merger), please visit the registration page on our website here.

- Common client – 5

- Exposure to other lawyers, either in support of the same client or on opposite sides of the same client, regularly leads to inquiries once a sufficient level of mutual respect and trust is established. Sometimes the common client will even make a recommendation that two lawyers or law firms combine their practices. (This was not the case with any of these five proposed mergers, but we include it as supplemental information because we see it from time to time.)

- Conversation between two law firm leaders – 3

- Managing Partners regularly interact with their peers (and those who don’t should find a peer group). We can think of several very large mergers that started with two law firm leaders sitting next to each other at a public conference or in one of our Managing Partner Roundtables, developing a personal relationship, and then exploring the broader possibilities.

- Referral from another consultant or a headhunter – 3

- Law firm merger negotiations is not a place to dabble or learn on the fly. Between my Partner (Joe Altonji) and me, we have 60+ years of experience in this field and we regularly receive referrals from others who make the introduction but cannot or should not try to create the deal. Some of these are sufficiently founded and developed to move forward in this stage.

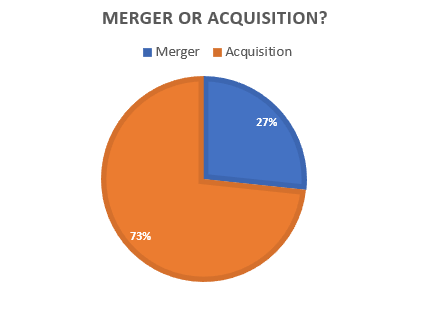

Was this a merger or an acquisition?

If you look at the publicly available data on law firm mergers, you will see that the vast majority of announced deals are acquisitions of a small entity by a much larger entity. In some data sets, the average size of the smaller firms is in the single digits so the categorization of “merger” is a true misnomer. Our data set reflects a similar result.

- 8 mergers – proposed transactions where both parties are larger than 50 lawyers and within a reasonable variance of each other on total size.

- 22 acquisitions.

What is the “success” rate (v1)?

There are two ways to look at “success” with respect to potential law firm combinations. Our preferred way is to look at the outcome in relation to what should have happened because, within the law firm merger world, NOT combining is sometimes (or often) the ideal outcome. If we look at outcomes against what (in our opinion) should have happened, the success rate from this sample is 89%.

-

- Three proposed transactions are still in progress and are not counted.

- Of the remaining 27, three solid, sound strategic deals that we favored and endorsed did not end up as a combination due to the inability of both firms to agree on “fine print” issues (e.g., the balance of seats in governance, performance expectations for Partners, firm name, etc.).

- All others ended up where they should have – 13 mergers and 11 amicable terminations to the discussions.

- Of the 11 terminated discussions, we stopped 6 of the deals at a time when either or both parties remained interested, but it was clear to us that a successful combination was not going to happen. The others ended via all parties reaching the same conclusion at roughly the same time based on the developing terms.

What is the “success” rate (v2)?

The second way to look at “success” is simply how many deals ended with a merger between two law firms (or the acquisition of one firm by another). Using this means for evaluation, the success rate from this sample is 48%.

- Three proposed transactions are still in progress.

- Of the remaining 27, 13 proposed transactions resulted in a formal combination.

Important note – this percentage may be overstated in relation to the general population of deals because any potential combination that becomes a negotiation project with us has a strong foundation and higher odds of success at the onset. Also, our decades of experience with mergers mean we’ve seen a LOT and can navigate the particularly tricky issues relatively well. Based on what we hear in the marketplace, a 1 in 3 success rate at this point in the process is typical. Still, there are many situations where the initial threshold tests for a potential deal were met, but where detailed discussions revealed more subtle reasons why a deal should not proceed, leading us to recommend the parties break off discussions, or for the parties themselves to reach the same conclusion independently. This accounts for the gap between the two ways of calculating “success.”

Who did LawVision represent?

When we are working on a law firm merger, we serve in one of the following three capacities:

- Counselor to the deal (30% of the transactions) – where we are acting for “NewFirm” and are working in the middle of the proposed combination, and for both parties, to see if we can create a term sheet that is good for all parties.

- Counselor to the acquiring party (33%) – where we are acting only for the larger firm of the two participants in the conversation.

- Counselor to the acquired party (37%) – where we are acting only for the smaller firm of the two participants in the conversation.

Statistically, based on our sample, 1 in 10 working concepts make it to a viable transaction and then one in two of our serious conversations (roughly) end up in a deal. In other words, a successful merger or acquisition requires an initial target list of 20+ viable candidates. Of course, this is an “average” outcome and each deal is different. A connection between two Managing Partners may be all that is needed for one firm while another may need 30 initial targets to find its “needle in the haystack.”

Mergers are used to accelerate the implementation of any law firm’s strategy or quickly address a critical need. In theory, a merger is much better and quicker than hiring a series of ones-and-twos. The reality is that there is a lot of frog-kissing in the process and merging two firms is extremely complicated. (We will explore why deals fail in an upcoming article.) Furthermore, with the ongoing consolidation in the industry, the number of viable deals/candidates for any interested party shrinks with every completed deal.

The purpose of this piece is not to discourage. Rather, it is to manage expectations carefully. While law firm merger negotiations are basically on hold right now (and rightly so), these activities will return and accelerate once an appropriate level of certainty is established and we shift to level 3 of our Recovery Playbook <link>. While we need to wait on the formal negotiations, some of the deals that will be negotiated then are being explored right now. The business of law and the evaluation of strategic opportunities never stop.

Now that you understand “the game” a bit more, good luck with your mergers and acquisitions!

To learn more about LawVision’s law firm merger and acquisition services or to register for our confidential, free merger marketplace, please visit our website here.

Posted In