Your Performance Orientation

In my last blog entitled Your Financial Performance Scorecard (link), I discussed four profit areas for law firms: (1) successful pricing and production, (2) effective financial hygiene, (3) balanced overhead and expense management, and (4) smarter reporting and signaling. In that blog, I also introduced the idea of a financial hygiene diagnostic scorecard to help tie these ideas together (to review this diagnostic, navigate here). In today’s blog, I will briefly discuss the opportunity for smarter financial reporting expanding on my comments from last time.

Challenges of Financial Reporting Today

Based on our research from our profitability and pricing surveys, many law firms have reasonably sound financial reporting processes in place, but there are common trouble spots:

Metrics Used May Sit on Shaky Foundations

Firms often use performance metrics that are narrow or built on a questionable foundation (this is not some nefarious activity but more typically a result of legacy report production, as in, we have always done it this way). The ability to get away with loose metrics has its roots in managing performance at the aggregate level, and sometimes it is due to political optics. Law firms have historically been able to manage profitability at the firm level because of wide profit margins. Consequently, if overall firm profitability is satisfactory, detailed metrics can be more loosely defined. But when margins compress (like they have been in recent years and will through the pandemic), metric precision becomes more important.

Take realization, for example. Ignore for the moment that realization is often confused as the dominant firm profit proxy metric (incorrectly most of the time). The bigger problem is that (1) firms focus too narrowly on a one-dimensional view of it (billed-to-worked value), (2) they frequently record discounts at the bill and are unable to separate real matter leakage from discounting practices, or (3) they don’t time-match the numerator (value captured) and denominator (value potential) which creates all kinds of trouble in reporting on the metric, especially as you narrow reporting periods. Realization metrics that suffer from these flaws cannot be used in an actionable way since they provide too much confusion in interpreting the results. The metrics lack credibility and can be used, at best, for broad-based reporting purposes.

Reporting Too Broadly with Little Insights or Actions

Standard financial reporting packages are often made up of broad statistics and measures with few recommended actions, placing the burden on the reader to figure out where to go next, which is challenging to do with broad data. The solution, however, isn’t merely providing more reader detail, but instead focusing on contextualizing and storytelling with the data. What is your call to action with the reader? What is the main message or takeaway? Think about ways to create standard reporting processes that focus on inspiring action and gaining insights using an action-driven approach.[1]

Reporting Post-Facto

Most financial reporting looks backward, with little attention to the future. Better reporting joins the past, the present, and projects to the future. It provides insights about the consequences or gains realized on the current pathway. It invites redirection, sharing of best practices, collaboration on successes, among other things.

Firms are becoming increasingly savvy and capable with modern reporting tools (e.g., Power BI, Tableau). The key is to project your message forward rather than backward. For example, rather than reporting matter leakage post-facto, consider presenting it in the context of work types, fee structures, key clients, and their impact on profitability this year or next. What patterns emerge? What happens if we don’t adjust? Where, when and how should we change? How does this impact our forecasting?

Disconnecting Reporting from Accountability

Reports that have no bearing on providing feedback, assessing performance, or calling on change provide limited effect and marginal organizational benefit. These discretionary reports are typically produced from standard processes with little thought towards change. Partners will readily know whether a report has teeth or not. Either redesign these reports or get rid of them – as they reduce credibility in the process.

Smart Reports

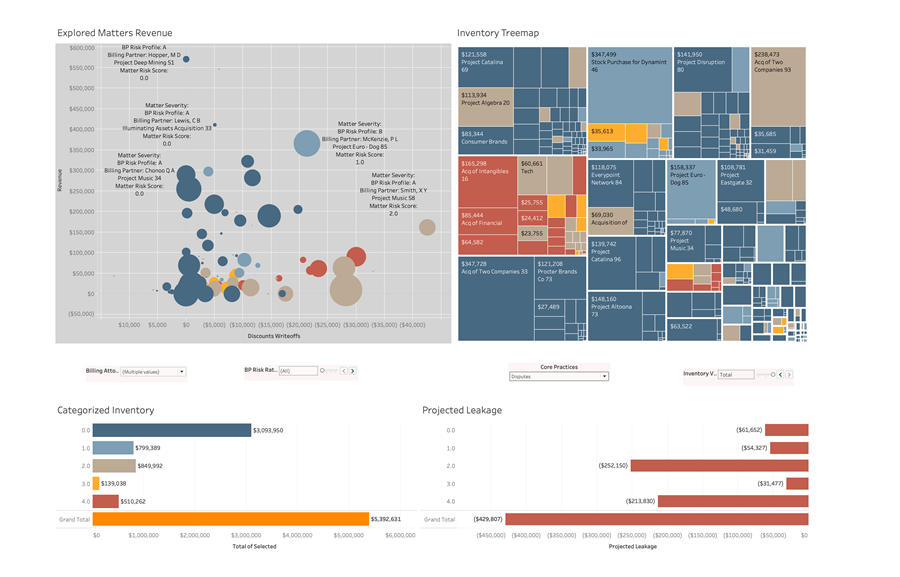

The ingredients of effective reporting include elements such as: maintaining purpose, focusing on key messages, creating clarity on issues, designing with elegance, and calling for action. But doing this takes thought and sometimes political courage. See below for an example of a graded inventory portfolio report. The report uses data to forecast risks associated with matters while predicting the timing and ultimate conversion of fee revenue. It provides a more realistic idea of the quality of your inventory, and it invites actions you can take to address problem areas.

Your Next Steps

Smarter reporting is available to all firms with purpose, focus, and the drive to produce change. But inertia and organizational routine often serve as roadblocks to more effective action-driven reporting. You don’t need fancy tools to improve your reporting but just the will and the persistence to put those reports into place. For more information about smart financial reporting, contact Mark Medice at mmedice@lawvison.com.

[1] For more information about this kind of reporting approach, see this website: storytellingwithdata.com. This website describes a simple but effective reporting process comprised of these steps: (1) contextualizing data, (2) visualizing it, (3) eliminating noise, (4) focusing and directing attention, and (5) putting it together via storytelling. These elements represent the building blocks of actionable reporting.